Ukrainian Metallurgy Is Losing Volumes in 2026: Why the Growth of Raw Material Exports Is a Warning Signal

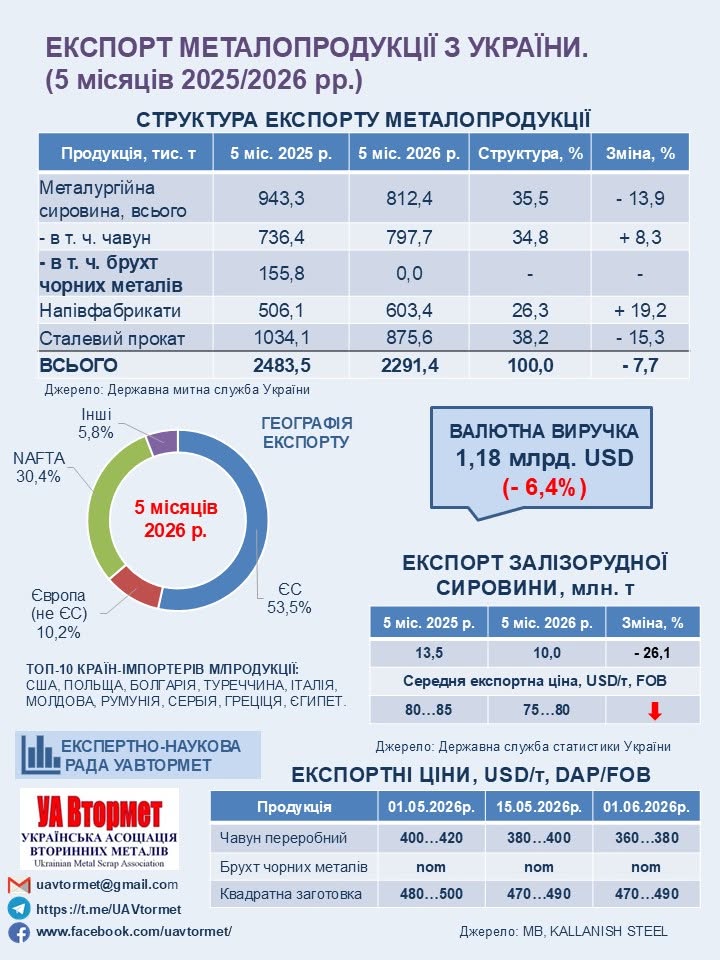

Ukrainian metallurgy in 2026 continues to work under pressure. In January-May, Ukraine exported 2.29 million tons of ferrous metals worth $1.18 billion. Compared with the same period last year, physical export volumes decreased by 7%, while foreign currency revenue fell by 6.4%. At first glance, the decline does not look critical. But the main problem is not only lower volumes. What is much more important is that the structure of sales is changing Ukraine is increasingly exporting raw materials and semi-finished products, while finished products with higher added value remain under pressure.

Time for Action analyzed what the latest data on exports and production of metal products show and why this dynamic matters for the entire economy. In the first five months of 2026, exports of merchant pig iron increased by 8.3% and amounted to 797.7 thousand tons. Shipments of steel semi-finished products grew even more noticeably by 19.2%, to 603.4 thousand tons. In other words, it is less deeply processed products that are showing growth. In the structure of ferrous metals exports, finished rolled steel still occupies the largest share 38.2%. But metallurgical raw materials have already almost caught up with it, with a share of 35.5%. Another 26.3% falls on semi-finished products, including square billets and slabs. This ratio is important. It is more profitable for the country to sell finished rolled steel than raw materials or semi-finished products. Finished products mean more processing inside the country, more work for enterprises, greater employment, a higher price per ton, and a stronger effect for industry. When the share of pig iron, billets, or slabs grows, the economy works more as a supplier of basic material for other countries’ production chains. The geography of exports shows that Ukrainian metallurgy remains strongly tied to Western markets. European Union countries account for about 53.5% of shipments. Another 30.4% goes to NAFTA countries the United States, Canada, and Mexico. European countries outside the EU account for about 10.2%, while other regions of the world receive 5.8%. This distribution has two sides. On the one hand, the EU and North America remain important sales destinations that support export revenue. On the other hand, high concentration in several markets makes Ukrainian metallurgists dependent on demand, logistics, trade rules, and industrial activity in those specific regions.

An even worse dynamic was recorded in exports of iron ore raw materials. In January-May 2026, Ukraine shipped 10 million tons of such products abroad. This is 26.1% less than in the same period last year, when exports amounted to 13.5 million tons. The decline in iron ore exports matters because ore is the base for metallurgical production. If raw material shipments are falling and steel and rolled products production are also declining, this points to a general weakening of the industrial cycle.

Domestic production also does not show stable recovery. In the first five months of 2026, pig iron output decreased by 0.6% to 2.99 million tons. Steel production fell by 6.1% to 2.875 million tons. Output of finished rolled products decreased by 6.7% to 2.34 million tons. The decline in steel and finished rolled products is the most revealing. Pig iron fell only slightly, while products at the next stages of processing are shrinking more noticeably. This confirms the same structural shift: metallurgy is preserving part of its basic production, but is holding weaker positions in segments where greater added value is created. The monthly dynamics also look uneven. In March, production grew noticeably in all three basic sectors pig iron by 22.5%, steel by 27.6%, and rolled products by 13.8%. But already in April there was a sharp decline pig iron fell by 16.1%, steel by 25.3%, and rolled products by 15.8%. This means that the industry is operating unstably. A single strong month does not turn into steady recovery. After March’s growth, April again showed weakness, while May only partially leveled the situation: pig iron and steel remained below last year’s figures, while rolled products showed a slight increase of 2.5%.

For the economy, this picture has several consequences. First, the reduction in foreign currency revenue means fewer inflows from one of the traditionally important export industries. Even a decline of 6.4% is noticeable when it comes to a sector that works with large volumes and matters for the balance of payments. Second, the growing role of raw materials and semi-finished products reduces the potential benefit for the country. Ukraine may sell significant volumes of metallurgical products, but earn less than it could with a stronger share of finished rolled steel.

Third, the fall in steel and rolled products production affects not only exports. It is also a matter of enterprise capacity utilization, employment, related industries, logistics, and tax revenues. Metallurgy does not exist separately: transport, energy, repair services, suppliers of raw materials, and equipment work around it. The main challenge for the industry is not simply to restore volumes. It is important not to lose the ability to produce and export products with higher added value. If the export structure continues to shift toward raw materials and semi-finished products, Ukraine risks locking itself into the role of a supplier of basic materials rather than a full-fledged producer of more complex metal products. The current data show that metallurgy is holding on, but its position is becoming weaker. Exports are declining, steel and rolled products production is falling, and growth in pig iron and semi-finished products does not compensate for the loss in the quality of the export structure.

Ukrainian metallurgy in 2026 is facing not only a decline in volumes, but also a dangerous structural shift. The growth of the raw material component may support part of exports in the short term, but something else matters for the economy preserving and strengthening the production of finished metal products, which provide more value, more jobs, and more resilience for industry.

About the Author

Related posts:

Stagnation After a Surge: What Is Happening to GМК Rail Freight and the Metallurgical Industry

Stagnation After a Surge: What Is Happening to GМК Rail Freight and the Metallurgical Industry  A New Trade Reality with the EU: What Has Changed for Ukraine’s Exports and Why This Is a Compromise for Both Sides

A New Trade Reality with the EU: What Has Changed for Ukraine’s Exports and Why This Is a Compromise for Both Sides  Ukrainian Ecommerce Is Growing but Losing Profitability

Ukrainian Ecommerce Is Growing but Losing Profitability  Scrap Metal Shortage in Ukraine: Why 2026 May Become Critical for the Industry

Scrap Metal Shortage in Ukraine: Why 2026 May Become Critical for the Industry